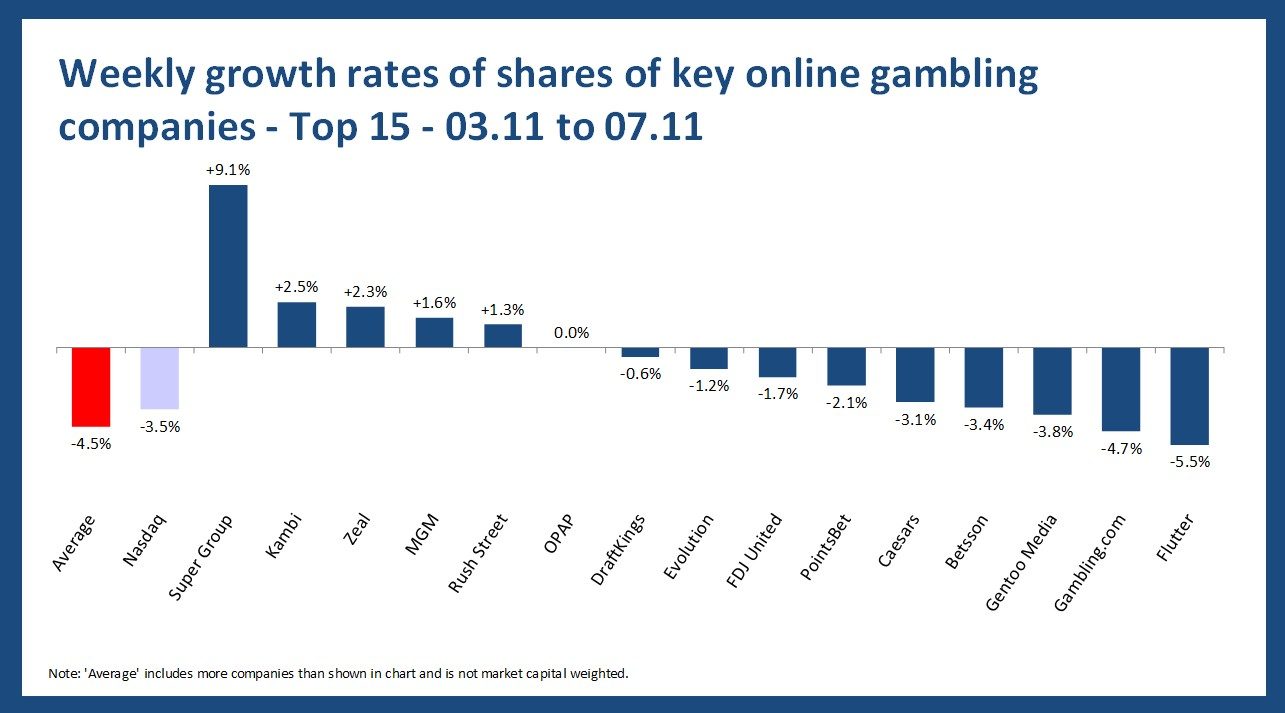

The recent analysis of online gambling stocks performance shows a mixed picture, with share prices declining by an average of 4% over the past week. While Super Group and Kambi stood out with gains of +9% and +3% respectively, several others, including Raketech and Evoke, saw double-digit losses. Overall, the sector underperformed compared to the Nasdaq Composite’s -3% decline, reflecting a generally weaker week for the industry.

Overview

- Average growth – On average, share prices analyzed decreased by -4% in the last week.

- “Winner” – The most significant leap in our sample of online gambling-focused companies was taken by Super Group with an increase of +9%, followed by Kambi (+3%).

- “Loser” – Raketech and Evoke had the worst weekly performance in our analysis, with a change of -15% and -13%.

- Comparison to the Nasdaq Composite – Compared to the development of the Nasdaq Composite (-3%), the average development of the online gambling industry looks “worse”.

Segment-specific developments

- Online-focused operators – The shares of online-focused operators included in the analysis saw, on average, a decrease of -1%; with Super Group (+9%) leading the ranking.

- Multi-channel operators – Among the multi-channel operators that also operate a relevant retail business, MGM is the “winner” with +2% while the average share development was -5%.

- Suppliers – The shares of the suppliers included in the analysis saw, on average, a decrease of -5%. The winner is Kambi with +3%

- Affiliates – On average, affiliates’ shares saw a decrease of -8% with Gentoo Media (-4%) leading and Raketech (-15%) coming last.

The share increase of Super Group

The sharp uptick in Super Group’s share price from 3 to 7 November appears to reflect the market’s positive reaction to its Q3 2025 report, which detailed record revenue and a significant increase in adjusted EBITDA.

The decline of Raketech shares

The sharp drop in Raketech Group Holding Plc’s shares between 3 and 7 November appears to stem from the company’s Q3 2025 earnings release on 6 November, which revealed a 42% year-on-year revenue decline and a continued slump in its paid-publisher network. Investors likely reacted unfavorably to the strong headwinds disclosed despite the firm’s emphasis on strategic cost-cuts and longer-term growth initiatives.

Please find more data and the methodology applied in the current edition of the OGQ Magazine. Also, find more content in our data section.