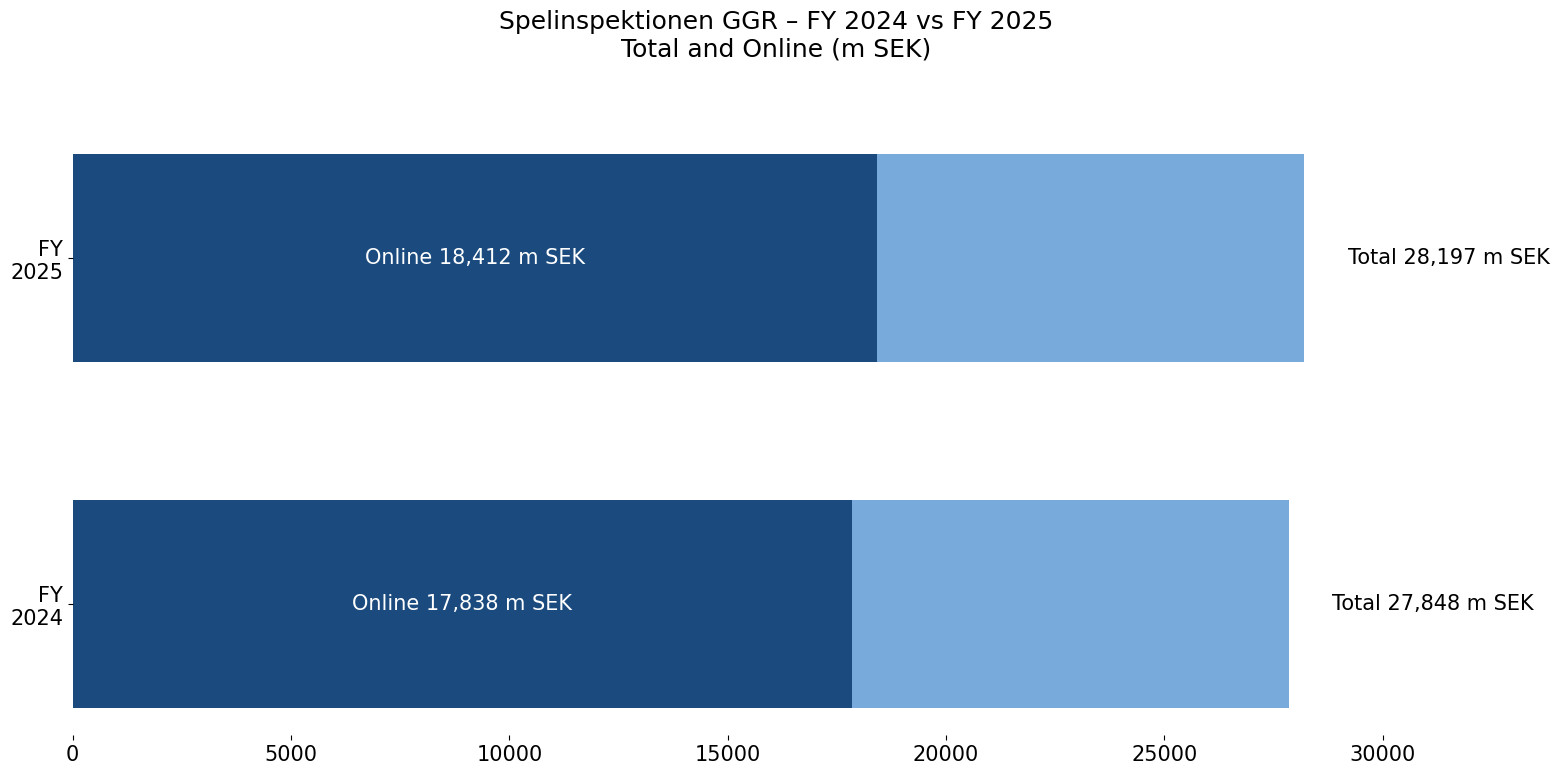

The Swedish gambling market 2025 delivered total GGR of SEK 28.2bn (ca. EUR 2.64bn) from licensed operators, compared with SEK 27.8bn (ca. EUR 2.6 bn) in 2024. The increase came mainly from online casino and betting, while land-based casino revenue continued to fall. See more details published by the Swedish Gambling Authority “Spelinspektionen“:

Commercial online gaming and betting generated SEK 18.41bn (ca. 1.7bn) in GGR in 2025, up from SEK 17.84bn (ca. EUR 1.67bn) in 2024. The vertical remains the dominant segment in the Swedish gambling market 2025. It accounts for roughly two-thirds of total licensed GGR (2025: ca. 65%; 2024: ca. 64%).

State lottery and cash machine games reported SEK 5.53bn (ca. EUR 0.52bn) in GGR in 2025, slightly below SEK 5.72bn (ca. EUR 0.54bn) in 2024. The segment’s overall share of the market edged down year-on-year. It remains the second-largest vertical by GGR.

State Casino Games (Casino Cosmopol) generated SEK 34m (ca. EUR 3.2m) in GGR in 2025, compared with SEK 160m (ca. EUR 15m) in 2024. The sharp decline reflects the continued contraction of the land-based state casino business. Its contribution to the Swedish gambling market 2025 is now marginal.

Games for public benefit, including lotteries, produced SEK 3.76bn (ca. EUR 352m) in GGR in 2025, slightly above SEK 3.7bn (ca. EUR 346m) in 2024. Hall bingo remained stable at around SEK 200m (ca. EUR 18.7m) in GGR. Combined, these activities maintained a steady share of the Swedish gambling market 2025.

Land-based commercial gambling generated SEK 263m (ca. EUR 25m) in GGR in 2025, compared with SEK 237m (ca. EUR 22m) in 2024. While still small in absolute terms, the segment recorded year-on-year growth.

Please find more news here.