Intralot reported a steady nine-month performance (Q1-Q3 2025) while completing the Intralot Bally’s acquisition. The move reshapes the business into a larger omni-channel supplier-operator. The company also adjusted guidance as integration and market conditions evolve, mentioning the Intralot Bally’s acquisition in its outlook.

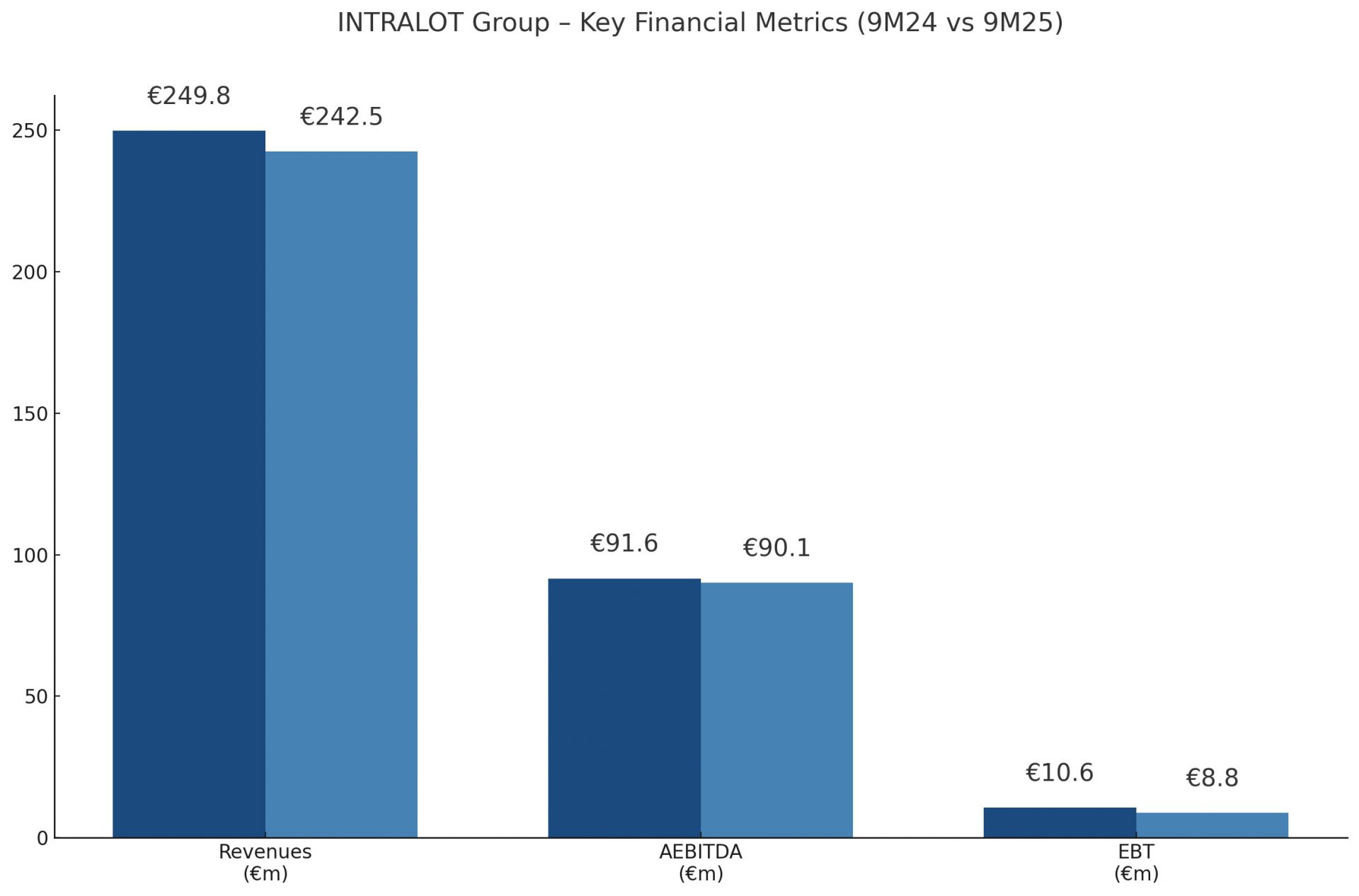

Group revenue reached EUR 242.5m, down 2.9% year-on-year, while AEBITDA stood at EUR 90.1m with a 37.2% margin. Net income after tax and minorities showed a EUR 3.1m loss, and EBT came in at EUR 8.8m. Lottery contributed 53.6% of revenue, followed by sports betting at 21.6% and VLT monitoring at 13.0%.

B2B/B2G (B2G means products/services directly supplied to government entitities or state-owned organisations) operations were stable, with constant-currency growth in the US of 2.3%, Australia of 3.9% and Argentina of 19.8%.

Operating expenses fell 16.1% to EUR 69.3m, driven by a 35% reduction in Turkey and lower US costs. Other operating income increased 4.8% to EUR 23.1m. Last-twelve-month AEBITDA reached EUR 129.3m, about 1.1% below full-year 2024.

Operating cash flow rose 5.9% to EUR 86.4m for the nine months, while net CAPEX (Capital Expenditures) dropped to EUR 20.4m. Free cash flow reached EUR 48.1m, supporting a EUR 56.9m reduction in adjusted net debt to EUR 298.8m. The company’s leverage ratio improved to 2.3x.

The Intralot Bally’s acquisition closed in October, combining the group with Bally’s International Interactive to create a €1.1bn-revenue business. Pro-forma nine-month revenue was EUR 790m with EBITDA of EUR 320m. CEO Robeson Reeves said the joined business “remains on track with its stated guidance” as it targets annualised revenue of EUR 1.07bn and adjusted EBITDA of EUR 435m.

Please find more news here.