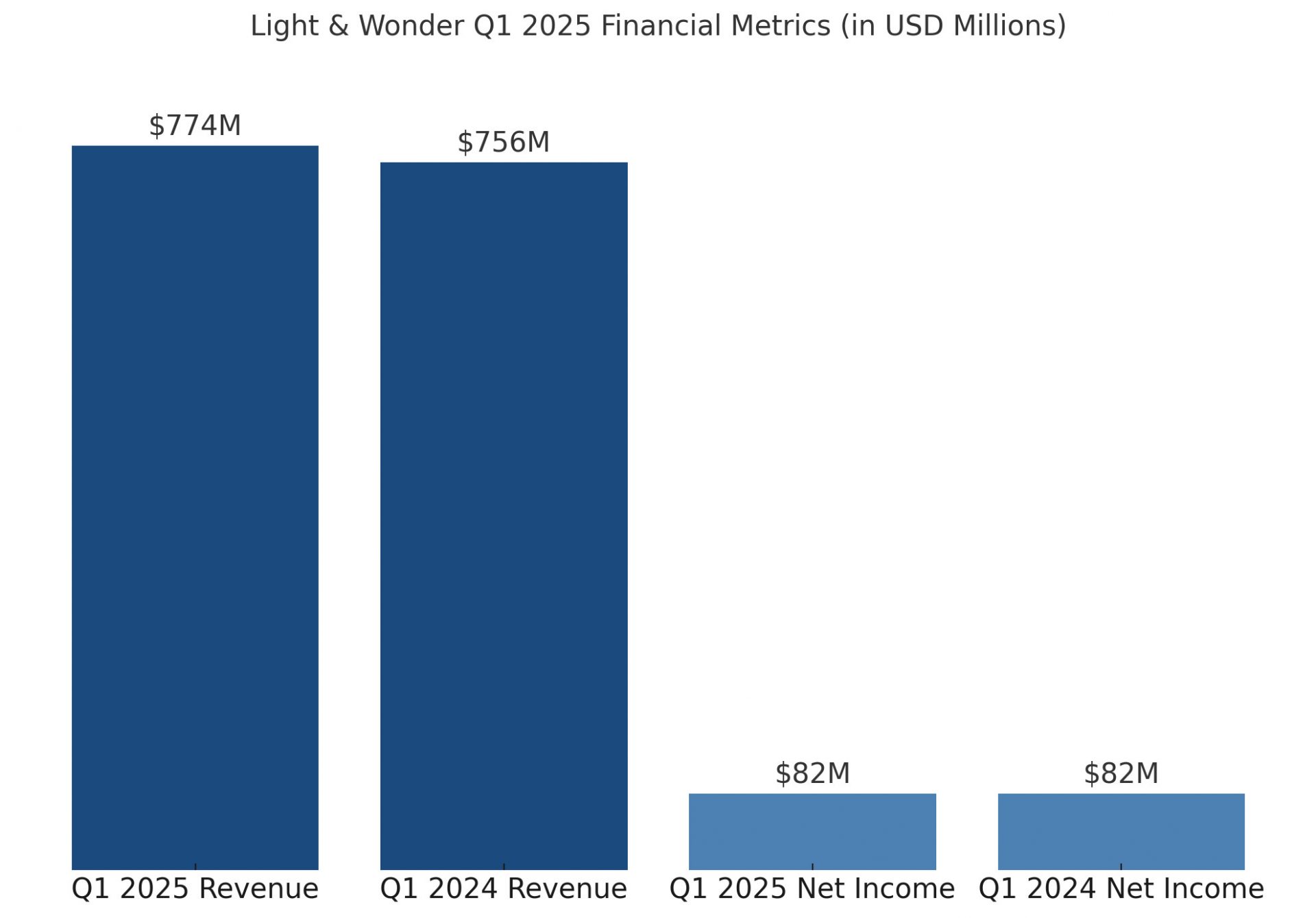

Light & Wonder earnings keep going up — that’s 16 quarters in a row now. The company brought in $774 million in Q1 2025, a 2% increase year-over-year. Their strong game lineup and solid player engagement helped fuel the results.

Gaming revenue hit $495 million, growing 4% from last year thanks to strong performance in table products, gaming systems, and operations. Installed gaming units in North America increased by 497 sequentially, now totaling 34,501. L&W kept its #1 ship share position in Australia and saw a 30% year-over-year jump in North America shipments.

SciPlay revenue fell 2% to $202 million, mostly due to fewer average monthly payers for JACKPOT PARTY Casino. Despite that, AEBITDA grew 3% to $64 million due to higher payer monetization and a 5% rise in ARPDAU to $1.06. The direct-to-consumer platform made up 13% of total SciPlay revenue.

iGaming revenue climbed 4% to $77 million, and AEBITDA jumped 8% to $27 million. Growth came from expanded partnerships and record-high platform wagers totaling $25.2 billion. Margin expansion added 100 basis points during the quarter.

Consolidated AEBITDA reached $311 million, up 11%, supported by higher gaming and iGaming revenues and improved margins. Net income remained at $82 million despite higher taxes and restructuring costs. Adjusted NPATA per share increased 21% year-over-year to $1.35.

Light & Wonder returned $166 million to shareholders via share repurchases, buying back 1.9 million shares. Net cash from operations grew to $185 million, while free cash flow improved to $111 million thanks to earnings and lower capital spending. CapEx was $61 million for the quarter.

The company is still on track to close its $850 million Grover Gaming acquisition in Q2 2025. The deal will expand L&W’s reach into five fast-growing U.S. states in the charitable gaming space. A new $800 million loan has been arranged to fund the acquisition.

U.S. and global tariffs on imports are expected to create near-term cost pressures. L&W is working on mitigation strategies like supplier diversification and cost controls. Despite this, they still expect to hit their $1.4 billion 2025 AEBITDA target (pre-Grover deal).

CEO Matt Wilson said, “We continue to see our omni-channel strategy prosper,” highlighting growth opportunities in game development and the Grover acquisition. CFO Oliver Chow emphasized their cash flow strength and operational efficiency.

Click here for more news.